Warren Buffett, Charlie Munger, and the Principles of Entrepreneurship

Over the years, I’ve invested hundreds of hours in trying to absorb the worldly wisdom of Warren Buffett & Charlie Munger. (Saved here are the best Munger / Buffett materials that I have come across– please feel free to read, learn and share!)

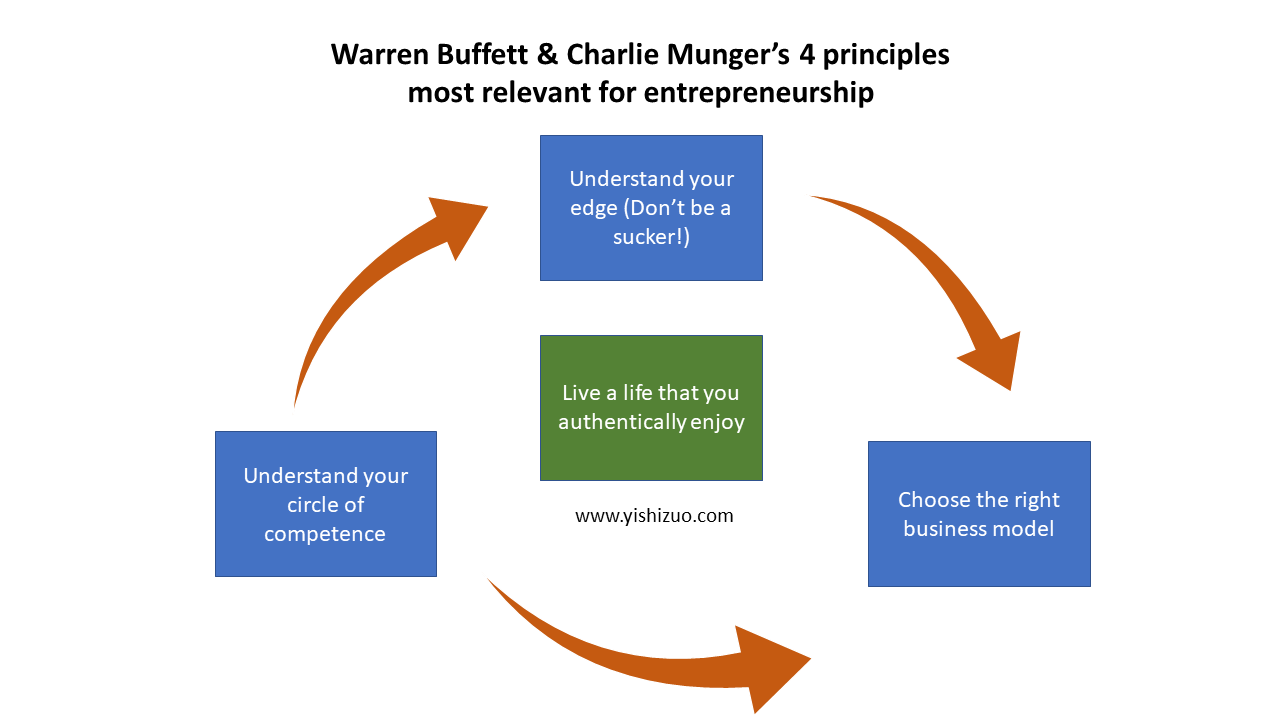

The core tenets of Buffett and Munger have profoundly shaped the way that I approach life, and below are 4 of their key principles that I believe are most relevant to entrepreneurship.

“Intelligent investing is not complex, though that is far from saying that it is easy. What an investor needs is the ability to correctly evaluate selected businesses. Note that word “selected”: You don’t have to be an expert on every company, or even many. You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.”

– Warren Buffett, 1996 Berkshire Hathaway Annual Letter

For entrepreneurs, our circle of competence comprises of all the resources that we have available.

Within one’s own circle of resources – somewhere, there needs to be some advantage. It doesn’t have to be a huge advantage. It could be as simple as one or two key insights – combined with your skills, your network, your reputation, and your energy.

Over time, we built on those limited resources that our start-up possessed, and our circle of competence grew to where we are today.

Buffett uses the following baseball analogy to reiterate this concept:

“We try to exert a Ted Williams kind of discipline. In his book The Science of Hitting, Ted explains that he carved the strike zone into 77 cells, each the size of a baseball. Swinging only at balls in his “best” cell, he knew, would allow him to bat .400; reaching for balls in his “worst” spot, the low outside corner of the strike zone, would reduce him to .230. In other words, waiting for the fat pitch would mean a trip to the Hall of Fame; swinging indiscriminately would mean a ticket to the minors.

. . .

In investing, I’m in a no-called strike business, which is the best business you can be in. I can look at a thousand different companies, and I don’t have to be right on every one of them or even 50 of ’em so I can pick the ball I want to hit. And the trick in investing is just to sit there and watch pitch after pitch to go by and wait for the one right in your sweet spot”

It’s clear to me that Buffet’s baseball analogy misses the mark for entrepreneurs, and it must be reinterpreted.

Where does a start-up’s circle of competence truly lie? There are so many rapidly moving pieces that make the boundaries of that circle very difficult to discern.

As entrepreneurs, we are forced to stretch the boundaries of our circle of competence far more frequently than investors are. Entrepreneurs don’t have the luxury of waiting for the perfect pitch in our sweet spot. A start-up must keep swinging and reaching for new opportunities. An entrepreneur must do things that do not feel comfortable.

I’ve personally learned to embrace the discomfort — that is the biggest mentality shift.

Entrepreneurs must sell our vision & capabilities to investors, the media, our customers and our employees. We must set stretch goals to motivate each of those constituents.

Unlike investors who are generally passive, entrepreneurs have the opportunity to create self-fulfilling prophecies. In fact, we must do so, otherwise we cannot grow.

Principle #2 Choose the right business model

Image credit: Garth von Ahnen http://www.artbygarth.com/

“‘I always used to tell [Bill] Gates that a ham sandwich could run Coca-Cola. And it was a damn good thing, too, because we had a period there a couple years ago where, if it hadn’t been that great of a business, it might not have survived.”

— Alice Schroeder quoting Warren Buffett in The Snowball (2008 Biography)

Note: Buffett disputes the context of this quote in a 2014 CNBC interview. However, I’m guessing that: 1) Buffett is backtracking in order to minimize offense and / or 2) The quote came from Charlie Munger if not Buffett, so I’ve decided to feature it with that caveat.

In any case, I think the sentiment is clear and makes logical sense. Buffett’s implicit advice is: Invest in businesses so good that morons can run them, so that you have an extra margin of safety.

To paraphrase another quote of Warren’s: When a great management team meets a tough business model, it’s the tough business model that wins. The business model is paramount.

“The single most important decision in evaluating a business is pricing power. If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business. And if you have to have a prayer session before raising the price by 10 percent, then you’ve got a terrible business.”

— Warren Buffett, 2011 interview with the Financial Crisis Inquiry Commission

As an entrepreneur, finding the right business model is easier said than done. Every market and every opportunity is slightly different. Micro-economics (i.e. customer acquisition costs, churn rates) matter. Customer personas matter.

You won’t know for sure whether your business model will work unless you invest resources to figure it out. A useful mental model to save some effort here is a concept from the investment world called “economic moats”.

If you think about it, the phrase “a start-up’s moat” is an oxymoron, given how vulnerable a young start-up is. However, to borrow a lesson from Peter Thiel’s book, From Zero to One : if you pick your market carefully, you can create your own tiny monopoly. Then over time, you use your monopolistic power within that niche to expand your moat and circle of competence.

Even if there are no barriers to entry today, a great start-up should have a credible path to creating barriers down the road.

Personally, with DeepBench, we’ve chosen a capital-efficient, network effect business model with SaaS and content components that should result in customer stickiness and a strong competitive moat in the long-run.

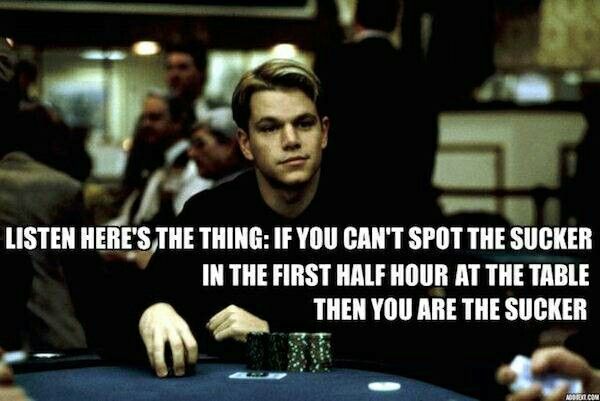

Principle #3 – Understand your edge and don’t be a sucker

Matt Damon’s quote above from Rounders is a poker aphorism that surfaced in the late 70’s and was used by Warren Buffett in the 80’s. This phrase has now become very popular in the investment world.

This concept is closely related to the circle of competence. The lesson here is that you have to understand what you are investing in. To bring up Buffett’s baseball analogy again: you don’t need to swing the bat unless a pitch is in your sweet spot.

Moreover, you need to know WHY the buying opportunity exists. If you think something is cheap, you better be able to explain why. Otherwise, you are the sucker at the table.

“If you play games where other people have the aptitudes and you don’t, you’re going to lose. And that’s as close to certain as any prediction that you can make. You have to figure out where you’ve got an edge. And you’ve got to play within your own circle of competence.”

— Charlie Munger, Art of Stock Picking

As mentioned in my previous article, inefficiencies exist in both the entrepreneurial and stock market worlds.

In the stock market, for every buyer, there is a seller. When you take an action, you imply that you see something that the market does not. As a stock market investor, it takes a dose of confidence bordering on arrogance to say that you are smarter than the market.

From a psychological perspective, this is the exact same “arrogance” that entrepreneurs must embrace when taking the plunge. You are more capable than the other entrepreneurs that have failed before you, and you are smarter than the incumbents in your industry that are somehow unable to act on this opportunity that you see. You are able to do something that people with more experience, connections, and capital cannot.

To determine where an entrepreneur sits along the boundary of calculated confidence vs. delusional arrogance, venture capitalists will often ask entrepreneurs some version of: “Why you? Why this team? Why now?”

I try my best to answer that question using the circle of competence framework. I strive to understand my own edge as well as Charlie & Warren do for themselves. And I aim not to be a sucker 😉

Principle #4 – Live a life that makes sense for yourself

Not too long ago, Warren Buffett was reading a 10-Q financial filing on a Saturday morning.

He then called the CEO of that company to ask a few questions.

The CEO replied to Warren, jokingly – “Is this what you do on Saturday mornings, read 10-Qs for fun?”

Warren replied matter-of-factly, “Yes”, and proceeded straight to his questioning.

I aspire to live a life such that my day-to-day business activities do not feel like “work”. I want my Saturday mornings to feel as equally enjoyable as my Tuesday afternoons.

I want to live life with a purpose. I want to voluntarily “work” weekends and evenings, even if I had enough resources to retire and live very comfortably for the rest of my life.

Over the decades, Warren Buffett has carefully arranged his life in a way that is catered to his own peculiar strengths and needs – in other words–his own circle of competence. I think that this is one of the most critical pieces to his success.

As an example, Buffett has famously described his management style as “delegation to point of abdication”– where he will often go months or even years without talking to some of his portfolio CEOs.

The environment that Buffett has thoughtfully crafted for himself affords him the freedom to do what he does best and what he most enjoys doing: Warren Buffett has ample uninterrupted time to read, think, and make decisions.

On a related note, Jeff Bezos espouses a very similar concept called work-life harmony. Bezos states that the word “balance” in the conventional terminology of “work-life balance” implies a trade-off, and that is a limiting way to think.

I agree with him.

Personally, I’m still in the process of figuring out what my own work-life harmony looks like. I do think that it is a lifelong process that requires constant reflection and adjustments, and I feel like I’m closer than I’ve ever been.

The implications of Buffett & Bezos’ life approach for entrepreneurs are clear.

Every entrepreneur is different, and every start-up is unique. We must choose a path that fits us—a path that is uniquely tailored to our strengths and weaknesses. We must craft an environment that is authentic to our working style and our life goals.

You don’t need to be a billionaire to start making tweaks to your environment and shifting your mentality. Success won’t happen overnight, but that is no excuse to not try.

Conclusion

If there is anything I’ve learned from Buffett and Munger, it is that their tenets are best considered holistically.

You can’t have happiness without work-life harmony.

You can’t achieve work-life harmony unless you understand your life goals and circle of competence.

Your circle of competence defines a) your edge and b) what business models make sense for you to pursue.

If you want to get better at these things, and whether you are an entrepreneur or not, my only advice for you is to read and reflect—and Buffett and Munger’s writings are a great place to start.

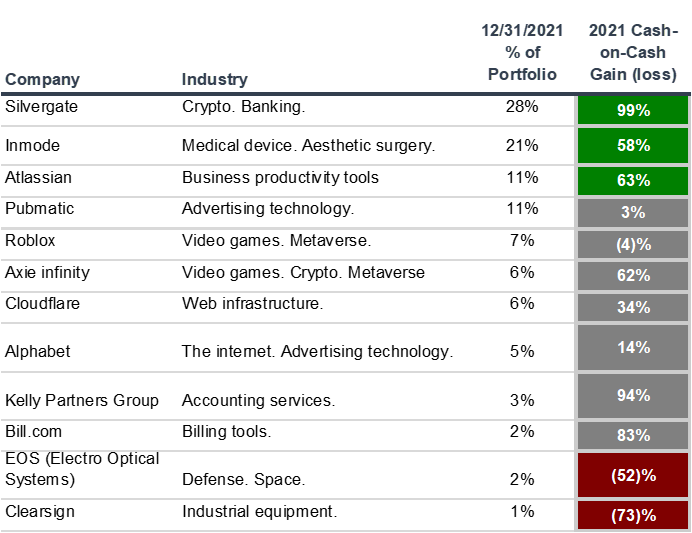

My portfolio returned 53% in 2021, vs. 29% for the S&P. Here is a closer look: Disclaimer: I am not a registered investment advisor. Nothing I write should be construed...

John Boyd was arguably the most brilliant military strategist since Genghis Khan. However, few have heard of him. Boyd was an iconoclast who revolutionized modern warfare, and his biography is...